In 2023, a mid-sized community bank received a Matter Requiring Attention from the OCC during its examination. The issue: the bank had not updated its fair lending risk assessment to reflect a new OCC interpretive letter published four months earlier. The letter was publicly available on the OCC website. Nobody on the compliance team had seen it.

Banking is one of the most heavily regulated industries in the world. A single community bank with $2 billion in assets might be directly supervised by the OCC, subject to FDIC deposit insurance rules, bound by Federal Reserve regulations on holding company activities, and required to comply with CFPB consumer protection standards. Add state banking department requirements, BSA/AML obligations, and evolving guidance on emerging topics like AI and digital assets, and the regulatory surface area becomes enormous.

The problem is not that this information is hidden. Regulators publish everything: enforcement actions, bulletins, guidance letters, proposed rules, final rules, and policy statements. The problem is volume and distribution. No single person can manually monitor the output of every relevant agency. And missing a single update can result in examination findings, enforcement actions, or fines that cost far more than any monitoring system.

This guide covers the regulatory landscape for banks, what specific pages and resources to monitor at each agency, how to set up automated monitoring with PageCrawl, and how to build a compliance team workflow that ensures nothing falls through the cracks.

The Banking Regulatory Landscape

Understanding which agencies publish what helps you build targeted monitoring rather than trying to watch everything.

Office of the Comptroller of the Currency (OCC)

The OCC supervises nationally chartered banks and federal savings associations. For national banks, the OCC is the primary prudential regulator.

What the OCC publishes:

- Bulletins: Formal guidance on supervisory matters, risk management, and regulatory topics. OCC bulletins are the primary channel for communicating expectations to national banks.

- Interpretive Letters: Responses to specific legal questions about bank powers and activities. These letters establish precedent and can affect how banks structure products and services.

- Enforcement Actions: Consent orders, cease and desist orders, civil money penalties, and formal agreements. Reviewing enforcement actions against peer institutions reveals regulatory priorities and common compliance gaps.

- News Releases: Announcements about policy changes, leadership updates, and supervisory initiatives.

- Comptroller's Handbook: Updated sections reflect evolving supervisory standards for specific banking activities.

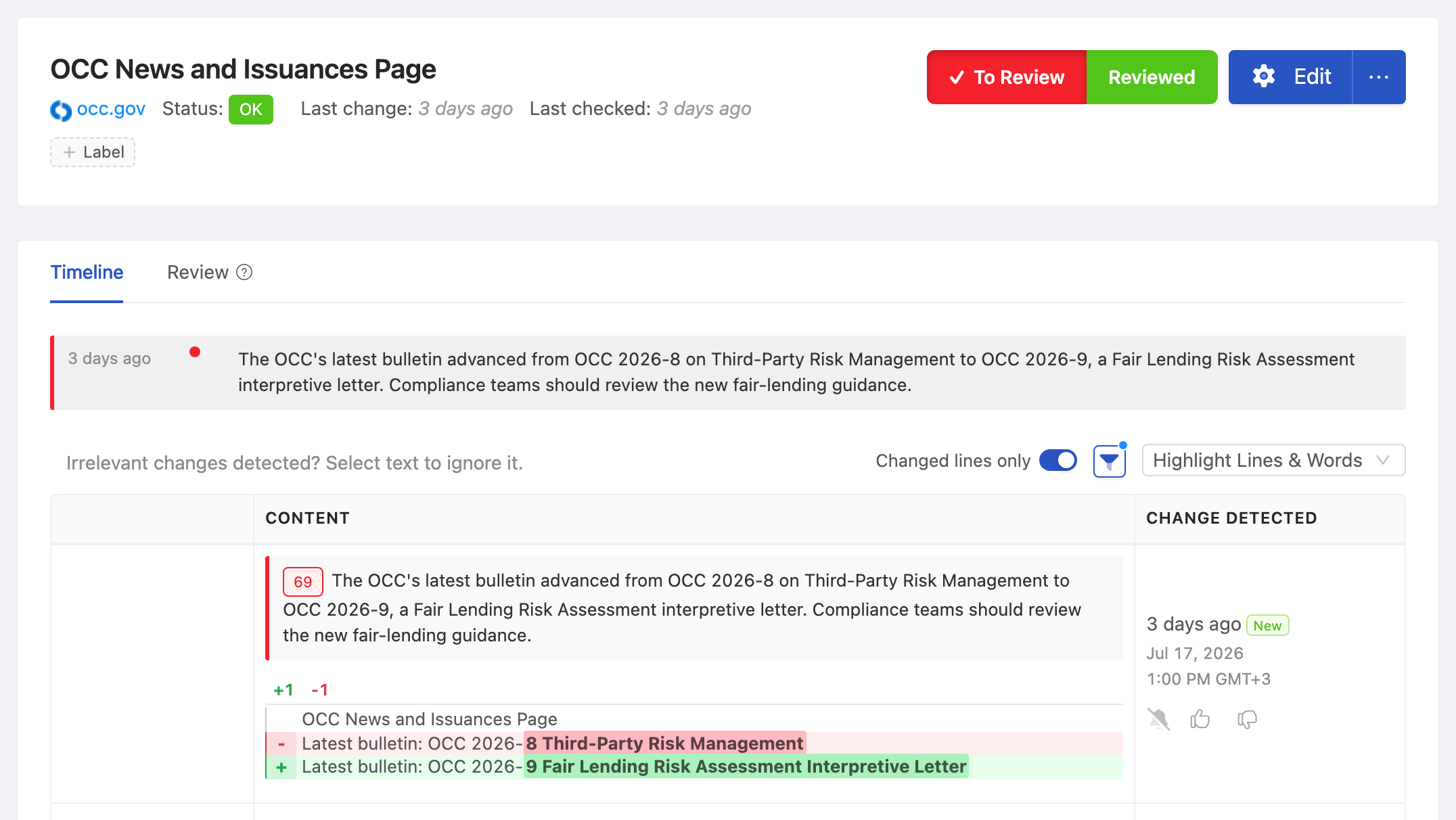

The OCC website (occ.gov) organizes this information across several pages. The "News and Issuances" section is the primary source. Bulletins appear at occ.gov/news-issuances/bulletins, and enforcement actions appear at occ.gov/topics/laws-and-regulations/enforcement-actions.

Federal Deposit Insurance Corporation (FDIC)

The FDIC insures deposits and serves as primary federal regulator for state-chartered banks that are not members of the Federal Reserve System. Even banks with other primary regulators are subject to FDIC rules regarding deposit insurance.

What the FDIC publishes:

- Financial Institution Letters (FILs): The FDIC's primary communication channel to supervised institutions. FILs cover regulatory changes, supervisory expectations, and compliance guidance.

- Regulations and Guidance: Proposed and final rules, advisory opinions, and compliance guides.

- Enforcement Decisions and Orders: Formal enforcement actions against institutions and individuals.

- Press Releases: Policy announcements, insurance fund updates, and institutional actions.

- Consumer Compliance Examination Manual: Updated sections reflect current compliance expectations.

The FDIC publishes FILs at fdic.gov/resources/financial-institution-letters. Enforcement actions appear at fdic.gov/bank-examinations/enforcement.

Federal Reserve System

The Federal Reserve supervises state member banks, bank holding companies, and increasingly, financial technology companies with banking charters. The Fed also sets monetary policy that affects bank operations.

What the Federal Reserve publishes:

- Supervision and Regulation Letters (SR Letters): Guidance to examiners and supervised institutions on supervisory expectations.

- Community Affairs Letters (CA Letters): Guidance on community development and CRA-related topics.

- Proposed and Final Rules: Published in the Federal Register but also announced on the Fed website.

- Enforcement Actions: Orders against supervised institutions and individuals.

- Speeches and Testimony: Governor speeches often signal upcoming regulatory priorities before formal guidance is issued.

- Beige Book and Financial Stability Reports: Economic and financial conditions that inform supervisory focus areas.

The Fed publishes SR Letters at federalreserve.gov/supervisionreg/srletters. Board actions and enforcement orders appear in the supervision section.

Consumer Financial Protection Bureau (CFPB)

The CFPB regulates consumer financial products and services. Banks with over $10 billion in assets are subject to direct CFPB supervision. Smaller banks must comply with CFPB regulations even though they are examined by their primary regulator.

What the CFPB publishes:

- Rules and Policy: Proposed and final rules on consumer financial products.

- Supervisory Highlights: Published quarterly, summarizing examination findings across the industry without naming specific institutions. These reveal where the CFPB is finding compliance problems.

- Enforcement Actions: Public enforcement actions with consent orders and civil money penalties.

- Guidance and Advisory Opinions: Interpretive rules, compliance bulletins, and advisory opinions.

- Complaint Database: Public database of consumer complaints. Trends in complaint data often precede regulatory action.

- Research and Reports: Studies on consumer financial markets that inform future rulemaking.

Note: The CFPB's regulatory posture and activity level can shift with administration changes. Monitoring the CFPB is important regardless of the current political environment, as existing rules remain in effect and enforcement can resume or intensify.

State Banking Regulators

Every state has a banking department or division that regulates state-chartered banks. State regulators publish their own guidance, enforcement actions, and regulatory changes. For banks operating across multiple states, the number of state regulators to monitor multiplies.

The Conference of State Bank Supervisors (CSBS) provides some aggregated information, but individual state regulator websites remain the primary source for state-specific requirements.

Other Federal Sources

Several additional federal sources affect banking compliance:

- FinCEN: BSA/AML rules, beneficial ownership requirements, and suspicious activity reporting guidance.

- OFAC: Sanctions programs and designation list updates. OFAC changes can require immediate action.

- Federal Register: All proposed and final federal rules are published here. The Federal Register is the official source, though individual agency websites are usually more accessible.

- FFIEC: Interagency guidance, IT examination handbooks, and BSA/AML examination manual updates.

Why Missing Updates Is Costly

The consequences of not catching regulatory changes extend beyond theoretical risk.

Examination Findings

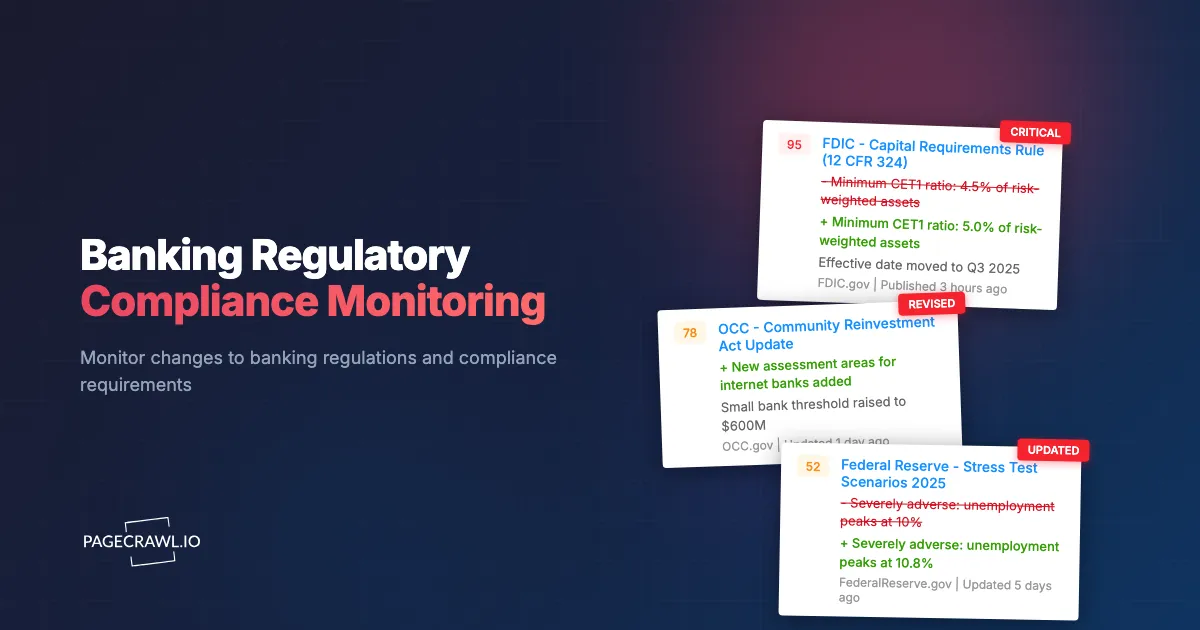

Bank examiners expect institutions to be aware of current guidance. During examinations, examiners assess whether the bank's policies, procedures, and practices reflect current regulatory expectations. When an OCC bulletin updates fair lending expectations and the bank's risk assessment does not reflect the update, that is a finding.

Findings come in escalating severity: observations, Matters Requiring Attention (MRAs), and Matters Requiring Immediate Attention (MRIAs). MRAs require formal remediation plans. MRIAs can restrict bank activities until resolved. Both consume significant compliance team resources and management attention.

Enforcement Actions

Repeated compliance failures or failure to address examination findings can escalate to formal enforcement actions. Consent orders, cease and desist orders, and civil money penalties are public. They appear on the agency's enforcement action page for anyone (including customers, counterparties, and potential partners) to see.

Financial penalties from enforcement actions range from tens of thousands of dollars for smaller violations to hundreds of millions for systemic compliance failures at larger institutions. The average cost of remediating an enforcement action, including legal fees, system changes, and ongoing monitoring requirements, typically exceeds the penalty itself by a significant factor.

Reputational Impact

Enforcement actions are public records. News coverage of banking enforcement actions is extensive. Customer trust, correspondent banking relationships, and acquisition opportunities can all be affected by public compliance failures.

For community banks, where relationships are fundamental to the business model, reputational impact from compliance failures can be particularly damaging.

Opportunity Cost

Compliance teams that discover regulatory changes late spend their time in reactive mode: rushing to assess impact, update policies, and implement changes under time pressure. Teams that catch changes early can plan methodically, allocate resources appropriately, and implement changes with proper testing.

The same regulatory change handled proactively over three months versus reactively over three weeks produces dramatically different outcomes in terms of quality, risk, and team stress.

What Pages to Monitor

Here are the specific pages and resources worth monitoring at each agency.

OCC Monitoring List

| Page | URL | Check Frequency | Why |

|---|---|---|---|

| Bulletins | occ.gov/news-issuances/bulletins | Daily | Primary guidance channel |

| News Releases | occ.gov/news-issuances/news-releases | Daily | Policy announcements |

| Enforcement Actions | occ.gov/topics/laws-and-regulations/enforcement-actions | Weekly | Peer compliance issues |

| Interpretive Letters | occ.gov/topics/laws-and-regulations/interpretive-letters | Weekly | Legal precedent |

| Comptroller's Handbook | occ.gov/publications-and-resources/publications/comptrollers-handbook | Monthly | Supervisory standards |

FDIC Monitoring List

| Page | URL | Check Frequency | Why |

|---|---|---|---|

| Financial Institution Letters | fdic.gov/resources/financial-institution-letters | Daily | Primary communication channel |

| Press Releases | fdic.gov/news/press-releases | Daily | Policy announcements |

| Enforcement Actions | fdic.gov/bank-examinations/enforcement | Weekly | Peer issues, priorities |

| Proposed Rules | fdic.gov/laws-and-regulations/proposed-rules | Weekly | Upcoming requirements |

Federal Reserve Monitoring List

| Page | URL | Check Frequency | Why |

|---|---|---|---|

| SR Letters | federalreserve.gov/supervisionreg/srletters | Daily | Supervisory guidance |

| Press Releases | federalreserve.gov/newsevents/pressreleases | Daily | Broad announcements |

| Enforcement Actions | federalreserve.gov/supervisionreg/enforcementactions | Weekly | Peer compliance |

| Board Actions | federalreserve.gov/aboutthefed/boardmeetings | Weekly | Regulatory approvals |

CFPB Monitoring List

| Page | URL | Check Frequency | Why |

|---|---|---|---|

| Rules and Policy | consumerfinance.gov/rules-policy | Daily | Rulemaking activity |

| Supervisory Highlights | consumerfinance.gov/compliance/supervisory-highlights | Weekly | Industry findings |

| Enforcement Actions | consumerfinance.gov/enforcement/actions | Weekly | Enforcement priorities |

| Blog/Newsroom | consumerfinance.gov/about-us/newsroom | Daily | Policy signals |

Additional Sources

| Page | Check Frequency | Why |

|---|---|---|

| FinCEN Advisories | Weekly | BSA/AML updates |

| OFAC SDN List changes | Daily | Sanctions compliance |

| Federal Register banking entries | Daily | Proposed and final rules |

| FFIEC guidance | Weekly | Interagency standards |

| State regulator bulletin pages | Weekly per state | State-specific requirements |

Setting Up Monitoring with PageCrawl

Here is how to configure monitoring for the pages listed above.

Choosing the Right Monitoring Mode

For regulatory pages, "fullpage" mode captures all content on the page. This is the right default for most regulatory monitoring because you want to catch any change, including new entries in lists, updated dates, modified text, and new links.

For pages with significant navigation and sidebar content that creates noise, "reader" mode (or content-only mode) filters to the main page content. This reduces false alerts from unrelated navigation changes.

Setting Up Agency Monitors

For each agency:

Step 1: Copy the URL for each page from the monitoring lists above.

Step 2: Add each URL to PageCrawl. Use "fullpage" mode for primary guidance and enforcement pages. Use "reader" mode for newsroom and blog pages where you only care about new posts.

Step 3: Set check frequency. Daily checks for primary sources (bulletins, FILs, SR Letters). Weekly checks for enforcement actions and secondary sources.

Step 4: Configure notifications to reach your compliance team. For most banks, email to a compliance distribution list ensures the entire team is aware. For larger teams, a dedicated Slack channel provides real-time awareness without clogging email.

Step 5: Organize monitors by agency using folders. An "OCC" folder, "FDIC" folder, "Fed" folder, and "CFPB" folder create a clean structure.

Handling Multi-Agency Monitoring

A typical community bank compliance team monitors 20-40 regulatory pages across agencies. At this scale, organization and notification routing become important.

Folder structure:

Banking Compliance/

OCC/

Bulletins

News Releases

Enforcement Actions

FDIC/

FILs

Press Releases

Enforcement Actions

Federal Reserve/

SR Letters

Press Releases

Enforcement Actions

CFPB/

Rules and Policy

Supervisory Highlights

Enforcement Actions

Other/

FinCEN

OFAC

FFIEC

State RegulatorsManaging Alerts Across Multiple Agencies

Volume management is the key challenge. With 30+ monitored pages, even with daily checks, alerts can accumulate.

Tiered Notification Routing

Not all regulatory changes deserve the same attention. Route alerts based on priority:

Tier 1 (Immediate): OFAC sanctions updates, FinCEN emergency guidance, anything from your primary regulator's bulletin page. Route these to Telegram or Slack for immediate awareness.

Tier 2 (Same Day): New bulletins, FILs, and SR Letters from any agency. Route to the compliance team email or Slack channel for same-day review.

Tier 3 (Weekly Review): Enforcement actions against other institutions, proposed rules in comment period, secondary source updates. Batch these for weekly compliance team review.

Assigning Review Responsibility

For compliance teams with multiple members, assign agency coverage:

- BSA/AML officer: FinCEN and OFAC monitors

- Consumer compliance specialist: CFPB and fair lending monitors

- Risk management: OCC bulletins, FDIC FILs, Fed SR Letters

- IT/Operations: FFIEC IT guidance, cybersecurity bulletins

Each team member reviews alerts from their assigned agencies and escalates significant changes to the group.

Compliance Team Workflow

Monitoring is step one. The workflow that processes alerts into action is what prevents examination findings.

Daily Alert Triage (10 minutes)

Each morning, the compliance officer reviews overnight alerts:

- Scan alert subjects for relevance to the bank's activities

- Flag items that require full review

- Dismiss routine updates (staff changes, non-relevant industry updates)

- Forward flagged items to responsible team members

This takes 10 minutes for a well-organized monitoring setup. The alternative, manually visiting each agency website every morning, takes far longer and misses more.

Impact Assessment (per significant change)

When a new bulletin, guidance letter, or rule is identified:

- Read the full text of the issuance

- Assess applicability: Does this apply to our bank's activities?

- If applicable: What is the effective date or expected implementation timeline?

- Identify affected policies, procedures, and systems

- Estimate remediation effort and assign responsibility

- Add to the compliance tracking system

This assessment converts a monitoring alert into an actionable work item.

Monthly Compliance Review

Monthly, the compliance team reviews:

- All regulatory changes identified during the month

- Status of in-progress remediations

- Upcoming effective dates for previously identified changes

- Monitoring coverage gaps (new regulatory topics or sources to add)

The monitoring history in PageCrawl provides the factual record of what changed and when, supporting audit documentation.

Archiving Regulatory Changes for Audit

Examination preparedness requires demonstrating that the bank monitored regulatory changes and responded appropriately.

Building an Audit Trail

PageCrawl's archiving capability stores snapshots of monitored pages over time. For regulatory pages, this creates a timestamped record showing:

- When a new bulletin or guidance was published (the date PageCrawl detected the change)

- What the page looked like before and after the change

- That the compliance team was notified (notification records)

During examinations, this audit trail demonstrates systematic monitoring. Rather than claiming "we monitor regulatory changes," you can show the system, the pages monitored, and the history of detected changes and responses. For compliance teams that need to preserve pages exactly as they appeared, PageCrawl can enable audit-ready WACZ archiving on request, creating self-contained, standards-compliant web archive files for each monitored page. WACZ archives are accepted as evidence in regulatory proceedings and can be stored in your document management system alongside other examination-preparation materials.

Document Retention

Regulatory examination cycles typically span 12-18 months. Maintain monitoring history for at least two full examination cycles (3 years recommended) to demonstrate consistent compliance monitoring over time.

For privacy policy and terms changes that affect compliance obligations, the same archiving approach provides evidence of when third-party terms changed and how the bank responded.

Scaling to State Regulators

Banks operating across multiple states face additional monitoring requirements.

State Banking Department Websites

Each state banking department publishes guidance, enforcement actions, and regulatory updates on its own website. The format and publication frequency vary significantly by state.

For a bank operating in three states, add the relevant bulletin or news pages from each state banking department to your monitoring. State regulators publish less frequently than federal agencies, so weekly checks are usually sufficient.

State Law Changes

State legislatures pass banking-related legislation that affects bank operations. Monitoring state legislature websites for specific bill tracking pages catches legislative changes, though the volume and format vary substantially by state.

For multi-state banks, legal counsel or a regulatory intelligence service often supplements direct monitoring with legislative tracking.

Common Challenges

False Positives from Page Layout Changes

Government websites occasionally update their page design without changing regulatory content. A page redesign triggers monitoring alerts even though no new guidance was published.

Using "reader" mode on pages with frequent design updates reduces this noise. Reader mode focuses on the main text content, ignoring navigation, footers, and layout elements that change during redesigns.

Pages That Use Complex Navigation

Some agency websites organize content behind search interfaces, filtering tools, or tabbed navigation. The landing page might not change when new content is published deeper in the site.

For these situations, monitor the specific listing page rather than the landing page. If new bulletins appear at a URL like agency.gov/bulletins?year=2026, monitoring that page catches new entries as they are added to the list.

Volume During Active Rulemaking

During periods of active rulemaking (which can follow administration changes, financial crises, or significant market events), the volume of regulatory output increases substantially. More frequent monitoring, faster triage, and temporary additional review capacity may be needed.

The monitoring system handles increased volume automatically. It is the human review process that needs to scale up during high-activity periods.

Beyond Web Monitoring

Web monitoring of regulatory pages is the foundation of a compliance monitoring program, but it is not the only component.

Federal Register API

The Federal Register provides an API that allows structured queries for regulatory documents. For compliance teams with technical resources, combining web monitoring of agency pages with Federal Register API queries provides comprehensive coverage.

Regulatory Intelligence Services

Commercial regulatory intelligence services (like Lexis, Wolters Kluwer, or specialized banking compliance services) provide curated and analyzed regulatory content. These complement web monitoring by adding expert analysis and cross-referencing.

Web monitoring with PageCrawl catches the raw changes. Regulatory intelligence services add analysis and interpretation. Together, they provide complete coverage.

Industry Associations

American Bankers Association, state banking associations, and specialized compliance organizations publish summaries and analyses of regulatory changes. Monitoring these organizations' publication pages adds an interpretation layer to raw regulatory monitoring.

Choosing your PageCrawl plan

PageCrawl's Free plan lets you monitor 6 pages with 220 checks per month, which is enough to validate the approach on your most critical pages. Most teams graduate to a paid plan once they see the value.

| Plan | Price | Pages | Checks / month | Frequency |

|---|---|---|---|---|

| Free | $0 | 6 | 220 | every 60 min |

| Standard | $8/mo or $80/yr | 100 | 15,000 | every 15 min |

| Enterprise | $30/mo or $300/yr | 500 | 100,000 | every 5 min |

| Ultimate | $99/mo or $999/yr | 1,000 | 100,000 | every 2 min |

Annual billing saves two months across every paid tier. Enterprise and Ultimate scale up to 100x if you need thousands of pages or multi-team access.

Compared to the cost of a single examination finding or remediation effort, regulatory monitoring is one of the cheapest controls a bank can run. Enterprise at $300/year covers 500 regulatory pages with full change history and timestamped screenshots, which is exactly the kind of documentation an examiner or auditor expects to see. Standard at $80/year works for smaller programs covering 100 pages across your primary federal and state regulators.

All plans include the PageCrawl MCP Server, so your compliance team can ask Claude to summarize every change to a specific rule or guidance document over the last quarter, pulling directly from your monitoring history and turning it into a queryable audit trail. AI assistants can create monitors through conversation on every plan, including Free.

Getting Started

Start with your primary federal regulator. If you are an OCC-supervised national bank, set up monitors for OCC bulletins, news releases, and enforcement actions. If you are an FDIC-supervised state bank, start with the FDIC FIL page.

Add your primary regulator's key pages (3-5 URLs) to PageCrawl with daily checks. Route alerts to your compliance team's email or Slack channel. Run this for two weeks to establish a baseline for alert volume and triage workflow.

Then expand: add Fed, CFPB, FinCEN, and OFAC pages. Add state regulators if applicable. Organize into folders by agency. Refine notification routing so alerts reach the right team members.

PageCrawl's free tier includes 6 monitors, enough to cover the most critical pages from your primary regulator. Standard plans ($80/year for 100 monitors) comfortably cover all federal agencies and several state regulators. Enterprise plans ($300/year for 500 monitors) support comprehensive regulatory compliance monitoring programs including state regulators, industry associations, and related compliance sources.

For a broader look at compliance monitoring software and approaches across industries, see the compliance monitoring software guide.

The cost of monitoring is negligible compared to the cost of a single examination finding. Systematic monitoring is not optional for banks. It is a regulatory expectation.