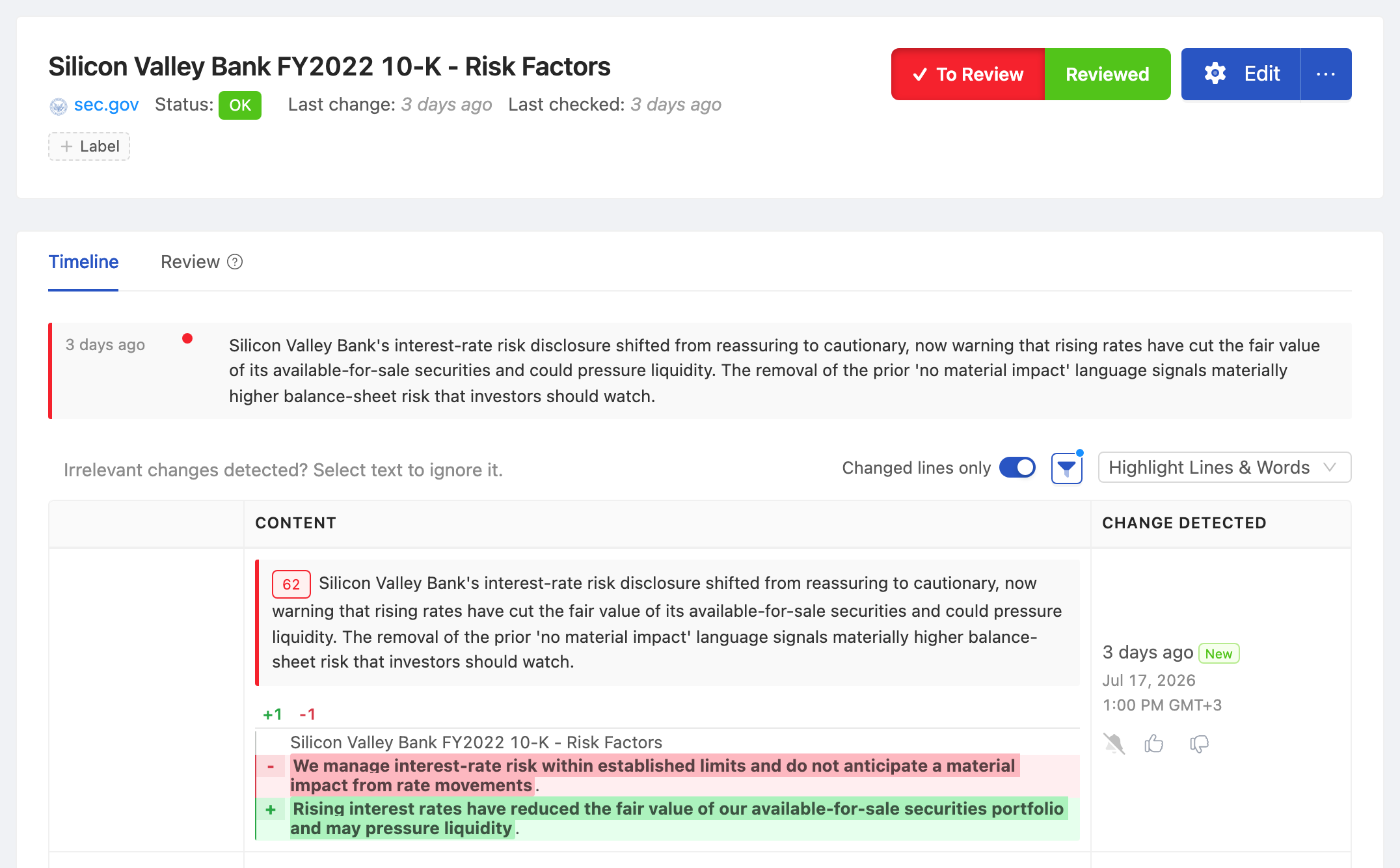

In its FY2022 10-K filed February 24, 2023, Silicon Valley Bank made subtle changes to the interest-rate risk section that had been present in the prior filing. The earnings press release made no mention of it. The conference call did not flag it. Anyone running a sentence-level diff on the filing against the prior 10-K saw the changes the same day the document hit EDGAR. Two weeks later, the bank failed.

The most under-read paragraphs in any annual or quarterly report are the ones that changed since last quarter. New risk factors, deleted disclosures, and amended MD&A language all signal what management and counsel are actually worried about, often before the conference call narrative catches up. Most analysts read the press release, glance at the income statement, and move on. The legal-drafted prose deeper in the filing is where the slower, more durable signals live, and it is precisely the part that most people skip.

This guide covers how 10-K and 10-Q filings appear on EDGAR, why filing-over-filing diffs are the highest-value reading of any quarterly report, and how to set up automated diff monitoring that surfaces the exact sentences that changed within minutes of filing.

Quick Setup

Enter a ticker to see a sample Risk Factors diff between the prior and current filing.

Why Diff 10-K and 10-Q Filings

Filing-over-filing diffs reveal information that does not appear in earnings press releases or call transcripts. The diff is interesting precisely because the standard quarterly cadence already filters out the obvious. What is left is the slow, deliberate language change that management and counsel signed off on.

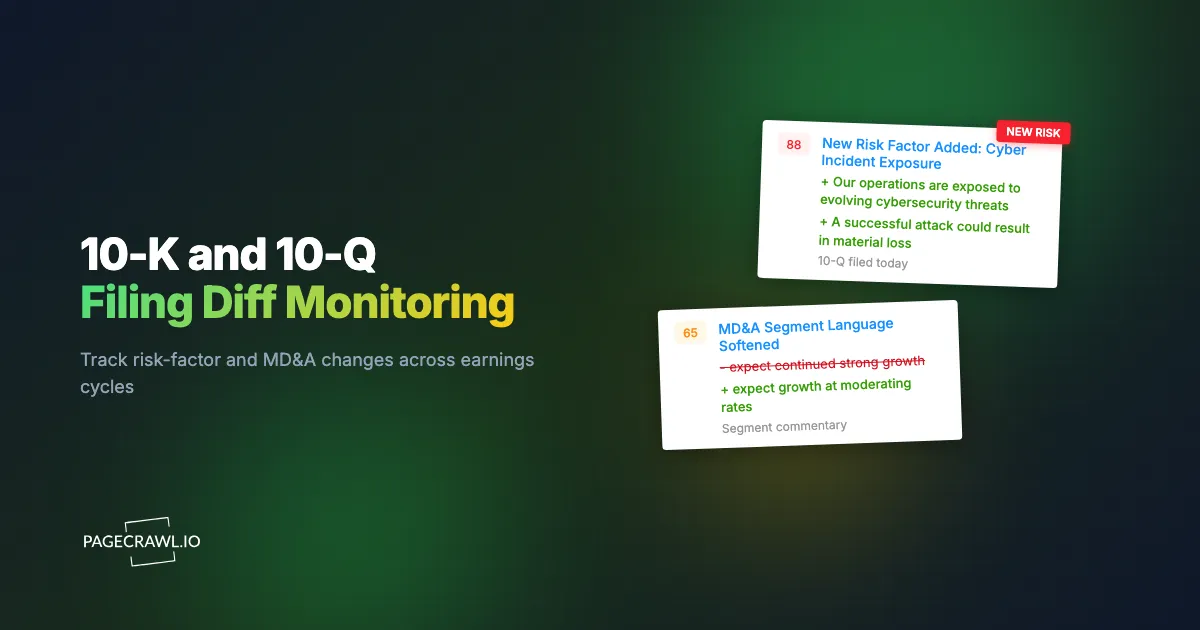

New Risk Factors Often Precede Material Events

When a new risk factor appears in a 10-Q, it means management or counsel believes a new material risk has emerged. The disclosure is often added defensively, weeks or months before the underlying risk becomes public. Academic research on 10-K risk-factor additions consistently finds predictive value for adverse stock returns over the following six months.

Removed Risk Factors Suggest Resolved Concerns

When a risk factor that appeared in the prior filing is removed, the implied signal is that management considers the underlying concern resolved or de-prioritized. This is the inverse signal and is sometimes more valuable than additions, because it can mark the end of a multi-quarter overhang.

MD&A Language Shifts Telegraph Segment Performance

Wording changes in MD&A discussion of specific segments, customers, or markets often telegraph segment underperformance one quarter ahead of the next earnings print. A move from "expect continued growth" to "anticipate near-term softness" is a small text change that carries significant disclosure weight.

Critical Accounting Policy Changes Foreshadow Restatements

Changes to critical accounting policies, especially in revenue recognition, lease accounting, or impairment testing, can foreshadow restatements or material impairments. These changes are buried deep in the filing and rarely covered by sell-side notes. A diff catches them on day one.

How 10-K and 10-Q Filings Appear on EDGAR

Each 10-K and 10-Q is filed on EDGAR on the company's filing index page, keyed by CIK (Central Index Key). The form-filtered URL patterns are:

https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK={CIK}&type=10-K&dateb=&owner=include&count=40

https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK={CIK}&type=10-Q&dateb=&owner=include&count=40Replace {CIK} with the ticker or 10-digit CIK of the company you want to track. A new filing appears as a new top row in the table. Each filing links to a filing index page that contains the full HTML version of the 10-K or 10-Q, plus exhibits and supporting schedules.

The full filing HTML is the document you want to baseline-diff. The first time you set up the monitor, copy the document link from the most recent filing and add it as a separate PageCrawl monitor. The next time the company files, PageCrawl diffs the new filing against this baseline and surfaces the exact paragraphs that changed.

Comparing Monitoring Approaches

| Approach | Cost | Latency | Diff Quality | Best For |

|---|---|---|---|---|

| Manual EDGAR refresh + Word compare | Free | Hours plus manual effort | Excellent if done | One or two priority names |

| Bloomberg Terminal FA/FB | $30K/year | Real-time alert | Filing-level only, no sentence diff | Institutional desks |

| AlphaSense (acquired Sentieo 2022) | $15K+/year | Minutes | Sentence-level | Sell-side and large buy-side |

| Calcbench | $5K+/year | Hours | Tagged-data focus | Quantitative research |

| PageCrawl on EDGAR | Free tier to $80/year | 5-15 minutes | Sentence-level via reader mode | Active analysts, retail investors, in-house counsel |

Sentieo and AlphaSense are the institutional default among equity research tools for sentence-level filing analysis and are excellent products. For a single analyst, a small fund, or an in-house counsel monitoring a focused coverage list, PageCrawl on the EDGAR filing pages does the same job at a fraction of the price.

Setting Up Filing Diff Monitoring in PageCrawl

Step 1: Find the company's CIK

Search the SEC EDGAR company search by ticker. The 10-digit CIK appears in the URL of the company's filing page.

Step 2: Add the filtered EDGAR filing page

Build the 10-K and 10-Q filtered URLs using the patterns above. Add each as a content monitor in PageCrawl. These pages catch the moment a new filing appears so you know to grab the new document link.

Step 3: Add the full filing HTML as a baseline

After each new filing, copy the document link from the filing index page (the main 10-K or 10-Q HTML, not exhibits) and add it as a separate monitor in PageCrawl. The next time the company files, the diff against this baseline shows exactly which paragraphs changed.

Step 4: Use reader mode for clean text diffs

Reader mode strips HTML chrome, page furniture, and most tables, focusing the diff on prose where risk factor and MD&A language changes live. This dramatically improves signal in the alert.

Step 5: Tag by section in folders

PageCrawl folders make it easy to organize monitors by section: Risk Factors, MD&A, Critical Accounting, Legal Proceedings. Per-section monitors are heavier setup, but they let you route Risk Factor diffs to one channel and Legal Proceedings diffs to another (useful when different teams care about different sections).

Step 6: Configure notifications

For analysts, email digests are usually the right channel; diffs are not minute-sensitive. For high-priority coverage, a Slack channel lets the whole team see the diff together. See the email alerts setup guide for delivery configuration.

Worked Example: Diffing a 25-Stock Coverage List

Take a sell-side analyst covering 25 names. The setup looks like this:

- Pull the CIK for each of the 25 tickers (about 15 minutes).

- Build the filtered 10-K and 10-Q URLs for each name (50 monitors).

- Use PageCrawl bulk import to add all 50 in one pass.

- After the first earnings cycle, add the baseline document URLs (another 25 monitors).

- Tag all monitors with

coverage-diffs. - Set 60-minute checks during earnings season, 6-hour checks off-season.

- Route alerts to a single

#filings-diffsSlack channel.

Total setup time: about 90 minutes for the first cycle, much less thereafter. Total cost: Standard plan at $80/year covers all 75 monitors with room to spare. The first time a sentence-level deletion in a risk factor leads to a positioning note before the rest of the Street notices, the cost recovers itself many times over.

Patterns Worth Watching For

New paragraphs in Risk Factors. A new risk factor in a 10-Q that did not exist in the prior 10-K or 10-Q is the highest-value diff signal. Read it carefully.

Sentence-level changes in MD&A. Discussion of specific segments, customers, or markets often shifts before the next earnings release. Wording changes in revenue or margin commentary are particularly informative.

Wording shifts that change legal weight. "Expect" to "may," "limited" to "material," "could" to "is likely to" all carry different disclosure weight. These are deliberate edits by counsel.

Deleted sentences. A previously disclosed specific issue that disappears from the new filing is often as informative as a new addition. The implied signal is resolution.

Changes in critical accounting policies. Revenue recognition, lease accounting, impairment testing, deferred tax treatment. Diff catches these on day one.

New related-party disclosures. Additions to related-party transaction tables or new disclosures of insider arrangements deserve attention regardless of size.

Combining Filing Diffs With Other Signals

The full value of 10-K and 10-Q diffs as buying signals shows up when you cross-reference them with other public datasets.

Combine with Form 4 insider trading. Pair filing-diff monitors with our Form 4 insider trading alerts guide. When new risk factors land in the same quarter that insiders are selling, the alignment is meaningful.

Combine with proxy compensation timing. Use our DEF 14A monitor to see whether MD&A language changes coincide with compensation structure changes.

Combine with 13F institutional positioning. Pair with our 13F holdings change monitor. When a sophisticated holder trims a position in the same quarter the company adds new risk factors, the alignment is informative.

Combine with press releases and IR pages. Add the company's IR press page as a sibling monitor. Sometimes a quietly added risk factor is followed weeks later by a press release that fleshes out the same concern.

Use Cases

Sell-side analysts. Diff each covered company's 10-Q within minutes of filing to feed model updates and the next-day note. Sentence-level diffs surface details that the press release glosses over and the call rarely covers.

Buy-side fundamental research. A library of historical diffs builds an audit-quality view of management's evolving stance. Long-term holders especially benefit from a multi-year diff archive on core positions.

Legal and in-house counsel. Compliance teams can flag new disclosures that may trigger D&O insurance review, securities-related risk review, or board-level escalation. For peer-company monitoring, diffs are the cleanest signal of evolving industry disclosure norms.

Short sellers. New risk factors and removed positive language are often the earliest written signals of thesis erosion. A diff archive across a short book is a daily research input.

Activist investors. Filings of target companies are read very carefully. A diff archive provides evidence trail for governance and operational concerns that may feature in eventual letters or proxy fights.

Financial journalists. Beats covering specific companies or industries use 10-K and 10-Q diffs as a continuous tip line. New risk-factor language often becomes a story before the next earnings cycle.

Frequently Asked Questions

How quickly do new filings appear on EDGAR? Filings appear on EDGAR within minutes of acceptance. The form-filtered listing page updates immediately. Your PageCrawl monitor catches the new row on the next check.

Can I diff against a specific historical baseline rather than the most recent filing? Yes. PageCrawl stores monitoring history per page; you can review the diff against any prior captured state. For long-term comparative analysis, the archive is part of the value.

What about 10-K/A and 10-Q/A amendments? Amended filings appear as separate filings with /A suffix. They can be monitored the same way and are often worth special attention because amendments imply something material was wrong in the original.

How does reader mode handle tables? Reader mode prioritizes prose. Critical accounting tables and exhibits are summarized rather than diffed in detail. For table-level monitoring, monitor the full HTML without reader mode; for prose-level monitoring (risk factors, MD&A), reader mode produces much cleaner diffs.

Do I need a paid plan? No. The Free plan supports 6 monitors, which is enough for a focused list of 2-3 priority names (filtered EDGAR page plus baseline filing per name). Standard at $80/year supports 100 monitors, which covers a 25-30 name coverage list comfortably.

Can the AI summary tell me what actually changed? Yes. PageCrawl's AI change summaries describe the diff in plain language ("Added new risk factor on data-center power constraints; revised MD&A language on cloud-services growth from 'strong' to 'moderating'"). This is the input to most analyst workflows.

Choosing your PageCrawl plan

PageCrawl's Free plan lets you monitor 6 pages with 220 checks per month, which is enough to validate the approach on your most critical pages. Most teams graduate to a paid plan once they see the value.

| Plan | Price | Pages | Checks / month | Frequency |

|---|---|---|---|---|

| Free | $0 | 6 | 220 | every 60 min |

| Standard | $8/mo or $80/yr | 100 | 15,000 | every 15 min |

| Enterprise | $30/mo or $300/yr | 500 | 100,000 | every 5 min |

| Ultimate | $99/mo or $999/yr | 1,000 | 100,000 | every 2 min |

Annual billing saves two months across every paid tier. Enterprise and Ultimate scale up to 100x if you need thousands of pages or multi-team access.

In event-driven strategies, minutes matter. One actionable signal surfaced before the broader market reacts can return more than a year of Ultimate. Standard at $80/year covers the core IR, press, and filings pages for a handful of positions. Enterprise at $300/year scales to a full watchlist. All plans include the PageCrawl MCP Server, so you can ask Claude to summarize every material change across a company's IR, press, and filings over any period you care about and get the evidence pulled straight from your monitoring archive. AI assistants can create monitors through conversation on every plan, including Free. Ultimate at $999/year adds 2-minute frequency and web archiving, which matters if you need provable timestamps for a thesis.

Getting Started

Pick a ticker, add the filtered 10-K and 10-Q EDGAR URLs as monitors, then add the full HTML of the latest filing as a baseline. Create a free account and the next quarterly filing will arrive with a clean diff against the last one.

Once you see the value, expand to a full coverage list of 15-30 names. The Standard plan at $80/year covers a serious coverage list with room for sibling monitors on IR press rooms and proxy filings. For analysts, in-house counsel, and active investors who treat sentence-level disclosure change as a real input to decisions, the cost recovers itself the first time a quietly added risk factor or deleted positive sentence leads to a position change or a board-level escalation.